After getting involved in the cryptocurrency and blockchain space, I’ve come to realize that two questions tend to dominate many conversations regarding this technology:

- What do you think the price of (bitcoin, ether, etc.) is going to be?

- When will we start to see mainstream adoption of cryptocurrencies?

As someone who often is at odds with the majority when it comes to pricing various cryptocurrencies and cryptoassets, I usually skip over the first question and move directly to the second,

“When will we start to see mainstream adoption of cryptocurrencies?”

Accurately forecasting the future adoption of a nascent technology is nearly impossible because it involves looking not just at the technology itself but the constantly shifting attitudes of those who would adopt it. However, we can fall back to an easier question, “What is necessary for cryptocurrencies to begin to achieve mainstream adoption?” Answering this new question is a more tractable problem because it ignores those conditions that may be sufficient for adoption and requires we identify only those that are necessary.

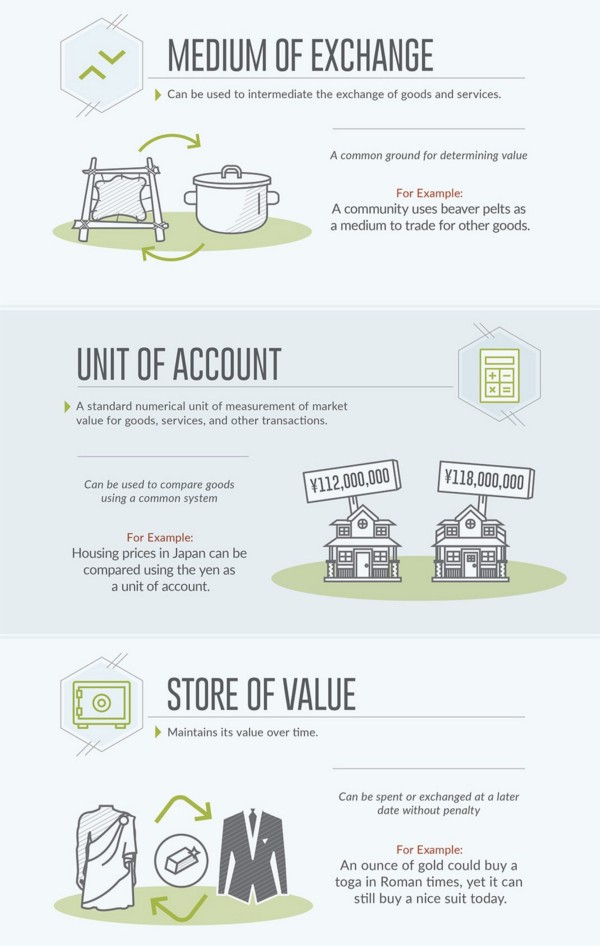

To put it bluntly, in order for cryptocurrencies to achieve broader adoption, they must be at least as good as those currencies against which they are competing.

Currencies are judged by their ability to serve three functions — as a medium of exchange, a unit of account, and a store of value. To successfully serve these functions, a currency must be easily and broadly usable (necessary for being a medium of exchange) and demonstrate at least some level of value stability (necessary for acting as a unit of account and store of value).

While both usability and stability must be improved for cryptocurrencies to compete on equal footing with fiat currency, I will focus solely on the latter in this post. If you’re interested in some exciting work being done to make cryptocurrencies more user friendly, there are plenty of projects such as uPort and Status to check out!

Back in 2014, Ethereum’s Vitalik Buterin published an article on potential ideas for a stable cryptocurrency. This post came less than a month after a group of researchers from Tokyo published their proposal for stabilizing the price of bitcoin. Since then, a few notable efforts to create a stable cryptocurrency have emerged or been refined. The rest of this post will focus on three of these.

BitShares’s SmartCoins

In 2013, Daniel Larimer launched BitShares, a well-hyped blockchain platform with many different components including DACs (Distributed Autonomous Companies), a decentralized exchange, and (most relevant to our current discussion) bitUSD, a cryptocurrency pegged to the US dollar and the platform’s first SmartCoin. Currently, Bitshares describes their SmartCoin concept as follows:

A SmartCoin is a cryptocurrency that always has 100% or more of its value backed by the BitShares core currency (BTS), to which they can be converted at any time, as collateral in a [contract for difference].

BitShares attempts to describe their stable coin using standard financial jargon, referring to contracts for difference (CFDs) and long/short positions. Unfortunately, such descriptions are neither useful as they do little to explain the actual steps involved nor accurate since the SmartCoin model deviates substantially from traditional CFDs. Instead of fancy terminology, let’s focus simply on the steps involved in the creation, exchange, and redemption of bitUSD:

- Suppose that Alice wishes to create $1.00 worth of bitUSD (1 bitUSD)

- To do so, she must lock away $1.00 worth of BTS plus some excess collateral amount to ensure that she has enough BTS locked away even if the price relative to USD drops.

- Once she has locked away this total amount, she receives 1 bitUSD from the BitShares network.

- Alice now sells this 1 bitUSD to Bob for $1.05 worth of BTS. Alice insists on charging Bob more than $1.00 because her collateral is at risk should the bitUSD/BTS price shift.

- Bob can redeem the 1 bitUSD he holds by submitting this request to the BitShares network. In such an event, the open position with the least amount of collateral covering its issued bitUSD (least-collateralized position) is forced to accept Bob’s bitUSD in exchange for an amount of BTS determined by the current price.

Having sorted through what’s happening, we first observe the major advantage of this system compared to custodian models — there is no counterparty risk. Since funds are locked by the network itself, there is no possibility that the alleged collateral isn’t there when a position is forced to close.

Unfortunately, there is a substantial drawback to using BTS to collateralize bitUSD. The risk lies in the possibility that the exchange rate between the dollar and BTS may move such that even the excess collateral held by the least-collateralized position is insufficient to cover what is owed. BitShares proposes that in such a black swan event, all open positions would be forced to close, purchasing back and destroying all outstanding bitUSD at the most recent price. Given the extreme and persistent volatility in cryptocurrencies, these black swan events would either be relatively common or extremely expensive to protect against, with average collateral coverage likely exceeding 150% when a new position is opened.

One could argue that such black swan events are, for the most part, a concern only until the BitShares system gains broad adoption. While this may be true (although even a smaller chance of an entire currency being automatically closed is concerning), it neglects the realities of how new products and technologies are adopted. Only a select few individuals and businesses are brave enough to adopt a new product (or currency in this case) on the promise that eventually it will be as safe as what they are already using. And since this group is unlikely to bring enough stability to the underlying BTS cryptocurrency to sufficiently mitigate the risk of black swan events, I believe that the bitUSD may be permanently stuck on the wrong side of the chasm, lacking the mainstream adoption it needs to become a viable currency.

MakerDAO’s Dai Stablecoin

MakerDAO was first introduced to the crypto world in the earliest days of Ethereum as a better way to achieve stability for a cryptocurrency. While they have yet to release their stable coin, the Dai, their ideas offer a notable improvement over alternatives. As with the bitUSD, here’s a simple stepwise overview of the system:

- Suppose that Linda wishes to create $1.00 worth of Dai (1 Dai).

- To do so, she must lock away $1.00 worth of an approved cryptocurrency, such as ether, plus a specified amount of excess collateral, determined so that the position is collateralized above the liquidation ratio.

- Once she has locked away her collateral, she receives 1 Dai from the Dai system.

- Linda now sells this 1 Dai to Tim for $1.05 worth of ether. Linda insists on charging Tim more than $1.00 because her collateral is at risk and she must also pay a mandatory stability fee.

The significant difference between the Dai system and those in the mold of the bitUSD is how MakerDAO’s system handles liquidation. Dai positions are only liquidated in the event that the position falls below the liquidation ratio for the collateral being used.

In such an event, the Dai system raises money to purchase the Dai associated with any under-collateralized position by selling MKR, the custodian and profit extracting token of system.

This is substantially different from bitUSD model, in which the collateral itself is used to close an under-collateralized position. In covering bad positions by inflating the supply of a third asset, MKR, the system is well protected from systemic black swan events during which all positions are forced to close and value is suddenly erased from holders of the stable coin.

Although better protected from black swan triggered collapses, the Dai system faces a more subtle and pernicious problem. To illustrate this problem, I pose the following question,

Under what conditions will people create Dai?

The answer to this question is perhaps misleadingly straightforward. People will create Dai either when they expect the price of the asset used as collateral to increase or when they can charge a sufficient premium to others for ensuring stability.

Put differently, we can conclude that obtaining Dai will become more expensive whenever expected demand for cryptocurrencies such as ether decreases. Conversely, obtaining Dai will be relatively inexpensive if the price of a collateral cryptocurrency is expected to rise. These statements, taken together, create a short term advantage and a long term disadvantage for Dai.

If MakerDAO only expects to bring the stability of fiat currencies onto the blockchain, the increasing cost of the Dai (as cryptocurrencies mature) may be acceptable as merely the cost of bringing this stability onto the blockchain. However, if the Dai ever aspires to challenge national fiat, this disadvantage will prove fatal.

The issue is that the Dai is cyclical with the economy at large (good currencies are countercyclical). Cryptocurrencies such as ether, and others likely to be used to collateralize the Dai, can be thought of as commodities with entirely inelastic supplies.

Cyclical → Unstable ← Positive feedback

Because of this, we expect their prices to fall when the economy contracts (or appears as though it may). These falling prices will trigger an increase in the cost of obtaining Dai, as already discussed. The increasing price of the Dai will increase the cost of capital, further harming the economy and resulting in a positive feedback loop of worsening economic conditions.

Seigniorage Shares

Back in 2014, Robert Sams of Clearmatics introduced the his stable coin proposal, Seigniorage Shares. While there has been no active work on the idea since early 2015 and are currently no planned implementations, I wanted to include it here because I believe it to be both the best explanation of the concepts behind a stable currency and the most promising design.

The concept behind Seigniorage Shares differs substantially from those approaches taken by BitShares, Stabl, and MakerDAO, as it involves no collateralized obligations or short/long positions with respect to some underlying asset. Seigniorage Shares works as follows:

- At time t(0), there is some number of coins, M(b), each worth $1.00.

- By time t(1), each coin has increased in value by 10% to be worth $1.10.

- The system now sells 0.1*M(b) new coins through an auction to individuals holding shares, destroying the shares it purchases.

- After the auction, the total number of coins in circulation is 1.1*M(b), driving the price per coin back to $1.00.

- At time t(2), the value of each coin is $0.90.

- In response, the system sells shares through an auction process to coin holders until the supply of coins has fallen to 0.99*M(b) through a buy/burn process.

- After the auction, the coin price again stabilizes at $1.00.

As we can see from this example, Seigniorage Shares proposal does not rely on collateral of any form and currency is a first-class citizen, rather than a derivative. This design protects the system the sorts of contagion that can bring down a derivative-based system and the simplicity it provides makes it more likely that the system will operate efficiently.

Blockchain technology has many potential uses, each with its own path to mass adoption, but its potential to be useful as a currency firmly depends on its ability to offer users a stable and reliable store of value and unit of account.

If you’ve enjoyed this article, feel free to comment and follow below!